Futures Market: Overnight, LME copper opened at $9,121/mt, initially bottoming at $9,117/mt. It then fluctuated upward, peaking at $9,219/mt by the session's end and closing at $9,217/mt, up 0.58%. Trading volume reached 18,000 lots, and open interest stood at 280,000 lots. Overnight, the most-traded SHFE copper 2503 contract opened at 75,450 yuan/mt, initially bottoming at 75,320 yuan/mt. It then climbed steadily, peaking at 76,080 yuan/mt during the session, before fluctuating rangebound at the close, ultimately settling at 75,900 yuan/mt, up 0.69%. Trading volume reached 40,000 lots, and open interest stood at 159,000 lots.

【SMM Copper Morning Brief】News: (1) The Ministry of Commerce and other departments issued two documents outlining subsidies for purchasing new mobile phones, tablets, and smartwatches (or bands), as well as plans for trade-in programs for home appliances in 2025. The documents specify subsidy categories and standards, with a maximum subsidy of 500 yuan per item for digital products like mobile phones and up to 2,000 yuan per item for 12 categories of home appliances. (2) US core inflation cooled, with December CPI up 2.9% YoY, meeting expectations, and up 0.4% MoM, slightly above market forecasts. However, core CPI YoY growth slowed to 3.2%, marking its first decline in six months and falling below both expectations and the previous reading. MoM growth of 0.2% also came in below expectations and the prior figure. Following the data release, traders moved up their expectations for the US Fed's first interest rate cut from September to July, with the total expected rate cut for the year rising from 28 basis points to 40 basis points, returning to levels seen before the non-farm payrolls report.

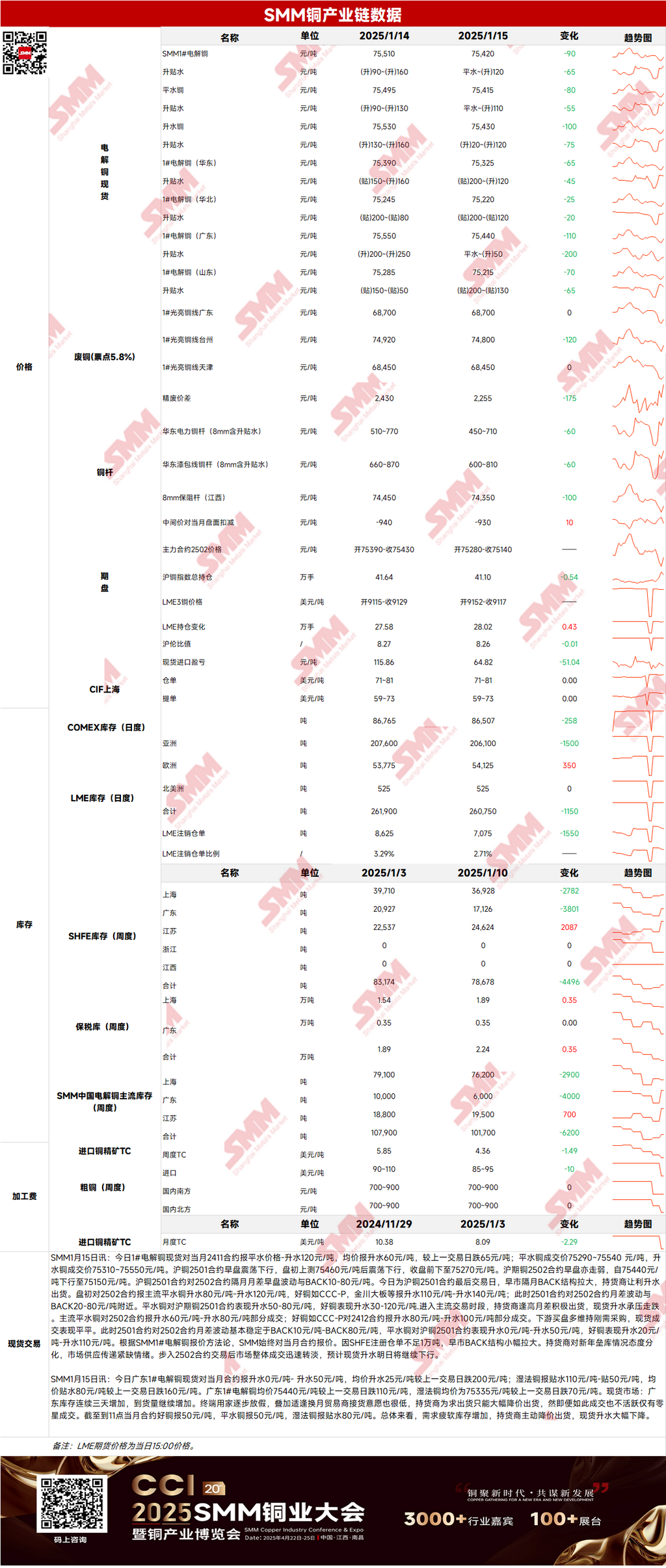

Spot Market: (1) Shanghai: On January 15, #1 copper cathode spot prices against the front-month SHFE copper 2411 contract ranged from parity to a premium of 120 yuan/mt, with an average premium of 60 yuan/mt, down 65 yuan/mt MoM. Due to SHFE registered warehouse warrants being below 10,000 mt, the early session backwardation structure slightly widened. Suppliers showed mixed attitudes toward year-end inventory buildup, and the market conveyed a sentiment of tight supply. After transitioning to the 2502 contract, overall market transactions quickly weakened, and spot premiums are expected to continue declining today.

(2) Guangdong: On January 15, #1 copper cathode spot prices against the front-month contract ranged from a premium of 0 yuan/mt to 50 yuan/mt, with an average premium of 25 yuan/mt, down 200 yuan/mt MoM. Overall, weak demand and rising inventories led suppliers to actively lower prices, resulting in a significant drop in spot premiums.

(3) Imported Copper: On January 15, warehouse warrant prices ranged from $71 to $81/mt (QP January), with the average price unchanged MoM. B/L prices ranged from $59 to $73/mt (QP February), with the average price also unchanged MoM. EQ copper (CIF B/L) prices ranged from $9/mt to $23/mt (QP February), with the average price unchanged MoM. These quotes referenced cargoes arriving in late January and early February. Recently, cross-market and exchange rate arbitrage opportunities have narrowed compared to earlier, weakening market buying interest. Suppliers actively sold late-month cargoes, but overall premiums remained high due to low inventories.

(4) Secondary Copper: On January 15, secondary copper raw material prices remained unchanged MoM. Guangdong bare bright copper prices ranged from 68,600 to 68,800 yuan/mt, also unchanged MoM. The price difference between primary metal and scrap was 2,250 yuan/mt, down 180 yuan/mt MoM. The price difference between primary and secondary copper rods was 1,510 yuan/mt. According to the SMM survey, despite the pullback in copper prices, many secondary copper rod plants reported receiving a few orders from terminal wire and cable factories this week. These companies plan to start their Chinese New Year holidays after the Little New Year, focusing on completing inventory orders before the holiday and not planning to build finished product inventories.

(5) Inventories: On January 15, LME copper cathode inventories decreased by 1,150 mt to 260,750 mt. On the same day, SHFE warehouse warrant inventories decreased by 246 mt to 9,484 mt.

Prices: Macro side, US overall CPI YoY growth mildly rebounded to 2.9%, while core CPI YoY growth unexpectedly slowed to 3.2%, below expectations. This eased concerns about accelerating inflation, leading traders to increase bets on a US Fed rate cut in June, with the likelihood of two rate cuts this year rising. Following the data release, the US dollar index briefly fell below the 109 mark, boosting overnight copper prices. Fundamentals side, year-end consumption weakened, and market transactions overall turned sluggish amid the contract rollover. In summary, after the US dollar index pulled back and recovered, copper prices are expected to face limited upside today.

》Click to View the SMM Metal Database

【The above information is based on market data and comprehensive assessments by the SMM research team. The information provided is for reference only and does not constitute direct investment advice. Clients should make cautious decisions and not substitute this information for independent judgment. Any decisions made by clients are unrelated to SMM.】